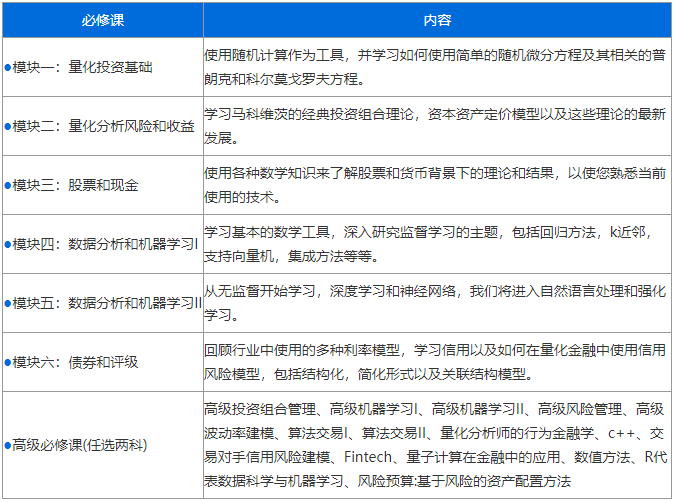

备考指南

备考指南

发布时间:2017-06-05

发布时间:2017-06-05

如何快速做好现金流报表,小编在此教大家一个关于CFA一级财务报表现金流量表贬值方法技巧。

在做现金流量表编制的相关题目时,对于新手而言,有时候很难一下子判断出各类资产负债表的增加或减少对于现金流量的影响。在这里,我们介绍三种不同的方法进行快速判断。

比如:应收账款增加100元,对于经营现金流的影响是增加还是减少呢?

CFA一级财务报表方法一:逻辑推算法

公司应收账款的增加说明别人欠本公司的钱增加了,换而言之就是本公司在当期应该有更多的钱但实际没有收到,因此是一种现金收入的减少。所以应收账款增加100元,体现在经营现金流量表中是-100元。

CFA一级财务报表方法二:基本公式法

基本公式:

Asset=Liability+Equity

变形公式:

Cash+non cash asset=Liability+Equity

Cash=-non cash asset+Liability+Equity

从上述公式,显而易见,非现金资产(红色部分)的增加对现金流产生减少的影响,而负债及权益(蓝色部分)的增加对现金流产生增加的影响。因此,应收账款增加100元,体现在经营现金流量表是-100元。

CFA一级财务报表方法三:口诀法

资产增加是花钱,现金减少用减号

资产减少是卖钱,现金增加用加号

负债增加是借钱,现金增加用加号

负债减少是还钱,现金减少用减号

对应上述口诀,应收账款增加100元,是资产的增加,代表现金的减少,因此在现金流量表中用-100来表示。

所以,你是否已经掌握了呢?以此种方式,就能很快的做好报表了。

分析CFA一级财务报表真题供大家学习:

CFA一级财务报表真题1:Under IFRS,company revenue should be recognizedwhen:

A.There is an evidence of arrangement between thebuyer and seller.

B.Cost can be readily measured.

C.The company receives cash flow from customers.

Solution:B

Under IFRS:risk and reward is transferred,nocontinuing control or management over the goods sold,revenue can be readilymeasured,probable inflow of economic benefits,cost can be realiably measured(for service,the stage of completion can be measured)Under GAAP:evidence ofarrangement between the buyer and seller,product being delivered or servicehas been rendered,price is determined or determinable,reasonably sure ofcollecting money.

CFA一级财务报表真题2:The company’s LIFO reserveat the end of 2010 is$1000 less than it at the beginning of 2010.If thecompany changes into FIFO method,the cost of goods sold at the end of 2010should:

A.Increase by$1000

B.Be no change

C.Decrease by$1000

Solution:A

COGSFIFO=COGSLIFO-△LIFO reserve=COGSLIFO+1,000

来源|金程 若需引用或转载,请联系原作者,感谢作者的付出和努力!

来源|金程 若需引用或转载,请联系原作者,感谢作者的付出和努力!

复制本文链接

复制本文链接 模拟题库

模拟题库

1693

1693